Why Your Inheritance Tax Allowances Are Worth Less Than They Look

Four of the UK's key Inheritance Tax allowances have not risen in decades. Here is what they are really worth today, and what it means for your estate planning.

Inheritance Tax allowances are set in cash terms. They are not indexed to inflation, so when the Chancellor leaves a threshold unchanged in the Budget, its real value quietly falls every year that follows. Four of the main Inheritance Tax allowances have not moved in a very long time, in one case for over fifty years.

The figures on the page look exactly as they always have. What they will actually shelter from tax has not.

The allowance today, versus what it should be

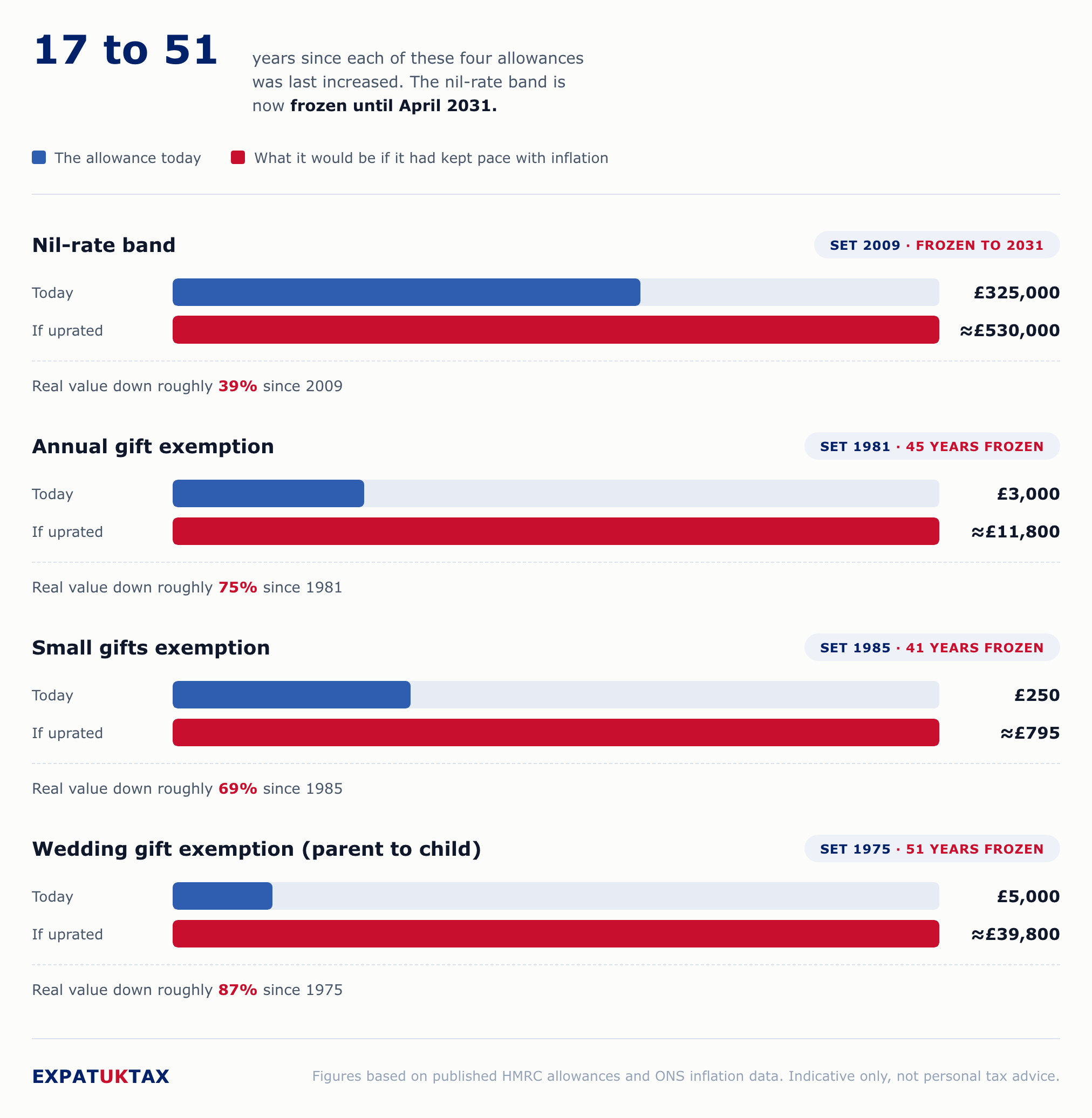

The nil-rate band

The £325,000 nil-rate band has applied since April 2009 (per IHTA 1984, Schedule 1, as amended). Had it risen in line with inflation since then, it would sit closer to £530,000 today, a real-terms reduction of roughly 39%.

This threshold has not simply stood still. It has been extended forward, meaning it will remain at £325,000 for years still to come. Combined with UK house price growth, this is the single biggest reason ordinary estates, not just wealthy ones, are increasingly drawn into Inheritance Tax.

The residence nil-rate band, a separate allowance for those passing a main residence to direct descendants, is frozen too. We have covered its £175,000 figure and the £2 million taper in our 6 April 2026 personal tax changes article.

The annual gift exemption

Every individual can gift up to £3,000 each tax year free of Inheritance Tax (per IHTA 1984 s.19). That figure was set in 1981. Uprated for inflation, it would now be close to £11,800, a real-terms fall of around 75%.

Unused annual exemption can be carried forward one tax year, but the underlying limit has not changed for 45 years.

The small gifts exemption

Small gifts of up to £250 per person, per tax year, are exempt regardless of who receives them (per IHTA 1984 s.20). This figure has been fixed since 1985. In today's terms it would be closer to £795, a reduction of about 69% in real value.

The wedding or civil partnership gift exemption

A parent can gift up to £5,000 free of Inheritance Tax on a child's marriage or civil partnership (per IHTA 1984 s.22). Grandparents can gift £2,500, and any other person £1,000. These figures date back to 1975, under the Capital Transfer Tax regime that preceded modern IHT. Adjusted for inflation, the parental gift allowance alone would now be close to £39,800, a fall in real value of around 87%.

Why this matters more for expats

For UK expats, this is not only a domestic UK issue. The Long-Term Resident (LTR) rules that took effect on 6 April 2025 replaced the old domicile-based test for Inheritance Tax. Individuals who meet the LTR conditions have their worldwide estate within the scope of UK IHT, not just their UK assets. We have set out the detail in our 6 April 2026 personal tax changes article.

That makes these frozen allowances more significant, not less. An expat's worldwide estate, gifting strategy, and use of trusts all sit against the same shrinking set of thresholds as everyone else's.

What you can do

- Model your position now. Our Inheritance Tax calculator gives an indicative estimate of exposure, useful as a starting point for a conversation, not a substitute for advice.

- Use the exemptions you do have, every year. A £3,000 annual exemption not used this tax year is not lost immediately (it can carry forward one year), but it cannot be banked indefinitely.

- Review lifetime gifting and trust planning. With allowances this far behind inflation, larger gifts increasingly rely on the seven-year rule rather than the small annual exemptions.

- Check your Long-Term Resident position. If you are a UK expat, your worldwide estate may be in scope even without a UK domicile.

If you would like to talk through what any of this means for your own estate, our Inheritance Tax planning service is a good place to start.